[rev_slider alias=”business”][/rev_slider]

Welcome to my website. As a United States Treasury licensed Enrolled Agent (EA) and Federally Authorized Tax Practitioner (FATP), it is my objective to provide you with valuable information about my background, qualifications, and the types of tax resolution services, assistance, and other tax-related services that I offer. I have included some important self-help links as well as technical discussions on a variety of topics.

We have launched a new website – www.dicknortontaxes.com – with more up-to-date content and an easier-to-navigate design. You may want to check it out.

Owe a lot of back taxes and want to take an international trip?

You will need to address your tax liability NOW because the IRS has been notifying the State Department to either deny (a new or renewal of) or revoke a passport if a taxpayer owes $62,000 (adjusted annually for inflation) or more AND meets other criteria. Read more about this relatively new tool Congress gave the IRS to deal with delinquent taxpayers here! Don’t book a trip abroad and then get a nasty surprise that you are unable to leave the U.S. because of a revoked passport!!

(This section for my clients contains copies of newsletters, highlights of tax law changes, and other items)

CLICK ABOVE IMAGE TO PLAY INTRODUCTION VIDEO

The 2025 filing season is over. If you filed an extension, you must file the final return by October 15th. Remember that the extension was only for filing. Any balance due must be paid by April 15th to avoid the accrual of interest and a late payment penalty.

If you have an outstanding liability that you wish to settle with the IRS by an installment agreement or an offer-in-compromise (OIC), the IRS requires taxpayers to be current with filing their returns, and in addition, to be current with making estimated tax payments for the current year or have sufficient withholding to cover the accrued tax liability on the earnings to date.

We can assist in getting any delinquent 2025 (and prior year) returns filed quickly to keep the accrual of penalties and interest to a minimum. With significant staffing losses, the IRS is increasing its use of artificial intelligence for identifying and auditing filed returns. It is important to be proactive and get help if you are notified of a pending audit or receive a notice of a balance due that you cannot pay in full. Many IRS actions are time sensitive. Do not ignore any correspondence you may receive. You could forfeit a valuable appeal right and find yourself subject to a lien or levy (the taking of your property by force).

Finally, be alert to fraudulent contacts from scammers posing as IRS employees!!! Thousands of taxpayers suffer financial loss and identity theft monthly when they provide information or make payments to these fraudsters!! Most of these crooks use scare tactics (like: there is a warrant for your arrest, or they are going to levy (attach) your accounts or your salary) if you do not pay immediately! They often demand payment by a weird method – such as gift cards or Western Union transfer. Almost always, the IRS’s first contact with a taxpayer will be a letter or notice regarding a pending audit or nonpayment of a liability. If you have never received such a letter or notice, then be very careful about an unexpected call allegedly from the IRS!

Bottom line: if you are surprised by a call from someone claiming to be from the IRS, get their name, employee number, title of their position, office address, and contact phone number, then tell them you will call them back after you have verified their information. You can then call the IRS at (800) 829-1040, and the employee can confirm whether you should have received the call and verify the employee’s information. If you cannot get through to the IRS, call me with the information, and I will check it out through my sources.

![]()

Click on the image above to visit the Blog

![]()

![]()

![]()

![]()

For Clients – Click Here to Make a Credit Card Payment

What will it cost me to have you prepare my returns (current or delinquent)?

While I suggest you read at least this main page of my website so you understand my background, you can click here to be taken directly to a page where you can provide me with your current year tax information that I can use in providing you with an estimate of the cost for me to prepare and e-file your personal or single-member LLC income tax returns. I do NOT do business (employment tax, partnership or corporation) returns, but I do have an associate who can provide that assistance. The professional software for business returns is expensive, and unless a preparer plans to do a significant number of those types of returns, it is not cost-effective to purchase it.

NOTE – I offer discounts on services to law enforcement, fire and military personnel – current and retired – in appreciation for your service to our community and our country. A number of my family members – including myself (US Army Security Agency – Pacific Command – during the Viet Nam era) – have served in one or more of these capacities, and I know the personal sacrifice they make and the risks they take in serving their communities and country!

| For my tax return preparation clients, please e-mail me for the 2023 organizers. I will get the website updated to include them soon. Prior organizers are in the FOR CLIENTS ONLY portion of this website. You will need the password to access this page. If you do not have it, please call or e-mail me, and I will provide the password. Note: the Obamacare penalties no longer apply to 2019 and later Federal returns. However, beginning in 2020, the State of California mandates that its residents have qualified health coverage (similar to the former Obamacare mandate), or penalties may be assessed on 2020 and later state returns. |

|

OFFERS IN COMPROMISE I wanted to say something about this topic, as it is the subject of numerous advertising claims by firms seeking to separate you from your money. The OIC program is tailored for those who are in dire financial straits and unable to fully pay what they owe through the sale of assets and monthly payments over the 10-year statute of limitations for collection of a balance due. It is a challenging process requiring not only well-prepared financial forms and supporting documents, but also a persuasive cover letter that can help secure an agreement to a lower tax amount to settle the account for less than what is owed. There are OIC “mills” that solicit clients and separate them from their money, without a glimmer of a chance of qualifying for an OIC. Any firm that promises to resolve your case for “pennies on the dollar” without a full, detailed, and thorough analysis of your financial situation should be avoided like the plague! The IRS issued an advisory notice in December 2021 that said the following: “We encourage eligible taxpayers in real financial distress to consider looking into an Offer in Compromise to resolve their tax issues,” said IRS Commissioner Chuck Rettig. “People also need to use caution with the program. Some companies routinely overstate how they can help with this program and clear up people’s back taxes for pennies on the dollar. A quick visit to IRS.gov can provide important information to help people with this program.” An Offer in Compromise allows you to settle your tax debt for less than the full amount you owe if you qualify. It may be a legitimate option if you can’t pay your full tax liability or if doing so would create a financial hardship. The IRS considers your unique set of facts and circumstances when making that determination. The OIC program serves an important purpose for a select group of taxpayers. The IRS periodically warns against hiring and paying needless fees to these “Offer in Compromise mills” that contort the IRS program into something it’s not and mislead people who have no chance of meeting the requirements while charging excessive fees, often thousands of dollars. OIC mills were listed in the last two annual IRS Dirty Dozen lists of tax scams to avoid. “I encourage taxpayers who may qualify for an Offer in Compromise to watch these videos and review information on IRS.gov to help them determine if the program is right for them,” Rettig said. “Don’t go to costly promoters advertising on television or radio who can make overstated claims or suggestions that the IRS will accept an OIC without even reviewing your situation first.” Bottom line – please be careful and do not get taken in by one of these OIC mill firms. If you want to know whether an OIC is an option for you, I will do a thorough analysis of your financial situation during a couple of hours of my consultation time to make that determination. As the Associate Chief in Los Angeles IRS Appeals before retiring from the IRS, I was the approving official for OICs for taxpayers within my jurisdiction. I can tell you if I would have approved an OIC for your situation if I were still in that position. If an OIC is a viable option and you retain me to represent you in pursuing an OIC (with the IRS or FTB), I will apply 1 hour of your consultation fee toward your retainer. I discuss the OIC program in more depth in the “Technical Issues” section of this website. |

NOTE – You will need the access code to download one of the organizers – contact me if you forgot it!

Also – the day to expiration for the filing deadline (which should be April 15th of the following year) is not working. If the 15th of April falls on a Saturday or Sunday, then the next Monday is the deadline.

At the outset, I want to alert everyone visiting this website that there are thousands of fraudsters trying to steal taxpayers’ identities or financial resources.

Please – do NOT give any personal information when receiving unsolicited calls from individuals claiming to be from the IRS or other government entities. If you are unsure of their alleged official status, feel free to get their contact information, then contact me, and I will validate the information provided. If you get a call from someone claiming to be from a financial institution and they ask you for identifying information, I suggest you get their information and then look up the customer service contact number on the Web, the back of your credit card, or your bank statement. Call that number and explain that you just received a call from someone alleging to be from their company. You MUST be very cautious during these challenging times – too many taxpayers are falling victim to these crooks!!

OK – I know that there is a lot to read on this website! But facing an IRS or state tax agency audit or collection action is serious business, and the more information you have, the greater your opportunity to successfully resolve a controversy. The vast majority of taxpayers who are caught up in an IRS or state tax agency process can face a significant financial hit (paying additional tax, penalties, and interest). However, if the errors or omissions were intentional (you need to understand that it is a very challenging task for the IRS Special Agent to develop such a case to the point where the U.S. Attorney would go before the Grand Jury for an indictment), in the worst-case scenario, the taxpayer could end up being confined to one of the Government’s lodging facilities for many years! Therefore, I suggest that you owe it to yourself to be as informed as possible as you wrestle with how best to deal with an actual or potential tax controversy. Tax Resolution Specialists – especially those with prior inside-the-IRS-job experience (in my opinion) – can be an invaluable resource in getting a client through the maze of tax compliance.

This is important. You can delegate the authority for return preparation to a professional, but the ultimate responsibility for its accuracy will always be yours!! Be sure you review your draft of the return carefully and ask questions if you do not understand something. Compare the current year’s return to the prior year and look for significant differences. If you have always owed money to the IRS or a state agency in the past, but this year you are getting a large refund, make sure you find out what changed to produce this result. Do not just blindly sign the return or e-file authorization. Further, if you are having your return e-filed, be sure you obtain from your preparer the evidence of agency acceptance!! There are numerous reasons why a return could be rejected – which is similar in effect to mailing your return without postage: it will be returned to you. The same scenario occurs with e-filed returns. Generally, they are processed, and the submitter is notified within 24 hours of its acceptance or rejection. You need proof of acceptance!!

Communicating with the IRS or State Tax Agency Employees

Taxpayers really need to exercise care when deciding whether to personally speak with IRS or state tax agency employees. In the worst-case scenario, making the wrong statement could turn what should have been a civil resolution into potentially a criminal tax matter. IRS Agents are well-trained to look for “badges of fraud” during their audits. Always be truthful in your statements to IRS or state employees. An intentional false statement or the provision of fabricated documents can land you in very hot water!

As a general rule, I advise clients not to volunteer information. If asked a question by an IRS Revenue Agent, Revenue Officer, TCO, or the equivalent state tax agency employee, answer it directly, clearly, but without unnecessary discussion. If you are approached by an IRS Special Agent (who carries a badge and a gun), my strong recommendation is to say nothing and immediately seek legal representation, as they are charged with conducting criminal investigations. A wrong statement to a Special Agent can lead to an indictment! A sharp tax attorney can best guide a taxpayer who is being pursued for a possible criminal indictment. If you are approached by a Special Agent and need a referral for a tax attorney, I have several I can recommend who were former IRS or US Department of Justice attorneys.

Should you handle your own controversy or audit?

At the outset, anyone facing a tax controversy, tax audit, or appeal can attempt to resolve their issues without professional help or guidance. In my 34+ years of IRS experience, I can say without hesitation that, in my opinion, the majority of taxpayers – whether individuals, partnerships, corporations, or other entity types – ended up with a better resolution or settlement when they were represented by professionals.

The IRS and State tax controversy resolution settlement process can be complicated. To be successful on their own, a taxpayer would have to devote a significant amount of time to studying the Internal Revenue Code, Regulations, case law, Rulings, and procedures. The Internal Revenue Manual (IRM – the “Bible” IRS employees must follow) and tax strategies for negotiating a favorable tax controversy resolution. Without this effort, I firmly believe that it is far more likely that a taxpayer will end up with a less favorable “deal” for himself or herself. Bottom line: the additional tax, penalty, and interest the taxpayer will ultimately have to pay may be significantly more costly in the long run than the actual cost of representation by a tax resolution specialist, who could have obtained a more favorable resolution. Not all accountants, attorneys, or enrolled agents offer tax resolution services. It is a specialized field of practice, and you really should seek the help of a tax resolution specialist if you are in a controversy – or potential controversy – with the IRS or a state tax agency.

When Do You Need Professional Help?

While I generally do not recommend that any taxpayer take on the IRS or a State tax agency on their own, I am very sensitive to clients facing financial challenges and may be able to suggest ways for them to get help and guidance while keeping their out-of-pocket costs down. For example, I have had a number of clients who were successful in resolving their IRS and other state controversies by having me “hold their hand” through the process, using my help in a consultative capacity. So, if you feel capable of and comfortable with working over the telephone, fax or mail (or, in rare circumstances – face-to-face) with an IRS Revenue Officer, IRS Revenue Agent, IRS Tax Compliance Officer (TCO), IRS Appeals Officer or IRS Settlement Officer, or any other employee involved in your IRS or California tax audit or collection controversy, then retaining me to hold your hand (which means that I will be providing you with an explanation of your options, strategic guidance, review of documents, and specific suggestions) could make the difference between the success or failure of your tax resolution efforts!

Let me stress this point again. I am not recommending that anyone who does not have a good understanding of IRS tax law, agency regulations, and procedures attempt to resolve their own tax controversy. Using the tax resolution services of a tax resolution specialist – and particularly one with extensive and successful IRS technical employment experience – is advisable based upon my experience.

Should I use my return preparer to represent me in an audit or collection matter?

As a general rule, I do not recommend taxpayers use the services of their current accountant or tax preparer to represent them in an IRS or state tax audit or tax liability negotiations – unless the preparer possesses special skills and extensive experience in tax controversy resolution. In my decades of experience, gleaned from almost 50 years of being both inside and outside the IRS, most accountants and preparers are very competent at return preparation, producing financial statements, and general accounting matters. However, providing a tax resolution service by sitting across the table from an IRS Revenue Agent, IRS Revenue Officer, IRS Appeals Officer, IRS Appeals Settlement Officer, or an IRS Tax Compliance Officer requires specialized knowledge of IRS audit, collection, and appeals procedures, policies, and practices. In my opinion, this is generally limited to those whose practice primarily focuses on providing tax resolution services. In my opinion, representatives who have had actual (and successful) inside-the-IRS experience will have the best opportunity to resolve their clients’ tax controversies with the least amount of financial consequences.

The IRS and all State tax agencies will only permit representation by individuals who are certified or acknowledged by a government agency as meeting the necessary technical (tax law and continuing education) qualifications. These individuals are Licensed Enrolled Agents (EA), Certified Public Accountants (CPA) or Attorneys. California has a special category of preparers with a title of CTEC. They have very limited authority to represent and, in my experience, a very small percentage have prior job experience within the IRS or a State tax agency. IRS employees who held technical positions (such as Revenue Agents, Revenue Officers, Appeals Officers, Settlement Officers, TCOs, and Special Agents) can automatically qualify for Enrolled Agent (EA) status, assuming their job performance met the high standards required for the license.

Potential Conflicts of Interest

Another factor to consider in deciding whether or not to retain your current accountant or preparer to represent you is whether there may be a possible or potential conflict of interest. The IRS and most state tax agencies can impose significant civil penalties against a preparer who negligently prepares a tax return. Consider this scenario. A preparer makes a mistake on a tax return, and the IRS is proposing to assess an accuracy penalty against the taxpayer (client). Rather than incur any monitory penalty for their error, the preparer (during his or her representation, say, in an audit….) may try to shift the Revenue Agent’s or TCO’s focus from himself or herself to the client as the underlying cause of the tax problem or tax issue – thereby resulting in the IRS imposing the accuracy or negligence penalty on the taxpayer/client rather than a preparer penalty on the preparer.

I have had success in obtaining client relief from potential penalties (such as the accuracy-related penalty) by persuading the Revenue Agent or TCO to assess the penalty against the preparer (generally much less in dollar amount) rather than the taxpayer as the underlying cause of the deficiency. Penalties are typically imposed for failing to properly account for an item of income, deduction, or credit on a tax return.

If the IRS proposes an accuracy-related penalty against a taxpayer, I would expect the taxpayer (client) to be curious about whether it was their mistake or their preparer’s. I have neither experienced (as an IRS employee) nor heard of a situation in which a preparer told a Revenue Agent, “That was my fault – hit me with the preparer penalty – my client should not be penalized.” I expect such a scenario would be rare. Multiple preparer penalties could lead to disciplinary actions by the Office of Professional Responsibility (OPR) – the IRS function that watches carefully over those individuals who practice before the IRS to ensure their actions are responsible and ethical. Therefore, preparers are very much aware that being subject to a preparer penalty could have far-reaching consequences beyond the basic penalty amount they would have to pay for their mistake.

Prepaid Tax Audit Protection

Speaking of preparer representation, some individuals and companies that prepare returns offer clients prepaid “income tax audit protection” for an additional fee as part of their return preparation package. This kind of representation – to my way of thinking – is much like an HMO arrangement. The individual or company has received their fee already, and there is, therefore, no financial incentive to make a sincere, effective effort to help their client get through an audit or collection matter with minimal financial burden – particularly in pursuing relief through the administrative appeal process. I have filed appeals and taken over client tax representation cases where the preparer-representative made a half-hearted effort to obtain relief for their client during the initial audit or collection process, but failed miserably. In many of those situations, proper representation at the first level (usually the Compliance Function within the IRS) would have resulted in resolution or settlement without the added cost of pursuing an administrative appeal.

Who are Enrolled Agents?

I occasionally get the question, “Who or what is an Enrolled Agent?“

Enrolled Agents are the only taxpayer representatives who receive their right to practice directly from the United States Government. Only Enrolled Agents must prove their competence in matters of Federal taxation and report their hours of continuing professional education (CPE) directly to the Internal Revenue Service (IRS). It is the individual states that license certified public accountants (CPAs) and attorneys; therefore, their licenses are state-specific. Unlike attorneys and certified public accountants, who may or may not choose to focus on taxes, most Enrolled Agents focus their practice on tax return preparation, and a smaller number on providing tax resolution services. A smaller percentage of Enrolled Agents also provide tax resolution services in tax controversy resolution, assisting their clients with audit and collection representation. Enrolled Agents (EAs) are tax professionals who are licensed by the U.S. Treasury and have demonstrated their competence by meeting that Department’s tough standards.

If you need my services to obtain a resolution of an IRS tax audit or State tax audit, an IRS collection controversy concerning secured tax debts, an IRS audit appeal, an IRS collection appeal, or any other tax-related problem with any income or employment tax agency, help is just an email or phone call away!

Time if of the essence in dealing with tax issues

With 34+ years of inside-the-IRS experience, I can assure you that the earlier you seek and receive help to resolve your IRS, California, or other state tax audit, tax collection, or other tax controversy matter, the sooner you can resume a normal life. An excellent analogy concerning a tax controversy is that an IRS tax audit and collection problem, along with those of the State of California tax agencies (FTB and EDD), and other State tax agencies, is much like tooth decay. It will just get worse if ignored. For example, a cavity that could have been fixed with a simple filling may end up requiring a root canal and a crown – or worse yet, an implant! Please be aware that when the IRS decides to perform a “root canal” on your personal or company finances or assets, they do not administer any anesthesia! It hurts! Further, recovery can take a very long time. Many taxpayers do not know that certain tax debts are ineligible for bankruptcy discharge (such as personal liability for their company’s failure to pay employment taxes – referred to as a “trust fund recovery penalty” – or, TFRP for short). That means that the taxpayer is burdened with the liability for a long time (typically 10 years, or much longer if the IRS opts to pursue a civil judgment against the taxpayer).

That is why if you are facing a tax controversy, I recommend that you make a decision TODAY to seek the tax resolution services of a tax resolution specialist licensed by a government agency as meeting tough standards for representation before your IRS, CA or State income tax or employment tax issues become so serious that they will require more effort (and cost) to resolve, or they result in significant financial consequences such as wage and bank levies, liens, or even seizure of your real or personal property.

An important note about tax liabilities

Tax liabilities are almost always secured debts. A federal lien arises after demand and non-payment of tax, including interest, additions to tax, and assessable penalties (§ 6321 Internal Revenue Code). The lien is affixed when the assessment is made and continues until it is satisfied or becomes unenforceable (§ 6322). The lien is not perfected against certain creditors until public notice is given (§ 6323), but timing of the secured interest still arises at assessment.

Issues surrounding the priority of liens and competing claims can be complicated, and advice and/or assistance from an attorney may be needed.

The services I provide regarding the resolution of liabilities relate solely to secured tax debts, and all references on this website to the resolution of Federal or State liabilities pertain to secured tax liabilities. If you have unsecured debts, such as credit card debt or personal loans, help is available from numerous attorneys or specialized debt-resolution companies to address these liabilities.

The IRS Fresh Start program may be able to help you pay your taxes

Are you struggling to pay your federal taxes? If so, the IRS’s Fresh Start program for individual taxpayers and small businesses may help. The IRS began its Fresh Start program in 2011 to help struggling taxpayers. In 2012, to help more taxpayers, the IRS expanded the program by adopting more flexible Offer-in-Compromise terms. This expansion enables some of the most financially distressed taxpayers to resolve their tax problems, possibly more quickly and at lower cost than in the past.

What is an Offer in Compromise?

An Offer in Compromise (known generally in the tax resolution industry as an “OIC”) is an agreement between a taxpayer and the IRS that settles the taxpayer’s tax liabilities for less than the full amount owed. Generally, the IRS will not accept an OIC if it believes the liability can be paid in full as a lump sum or through a payment agreement. The IRS looks at the taxpayer’s projected future income and the net realizable value of current assets to make a determination of the taxpayer’s reasonable collection potential. OICs are subject to acceptance based upon meeting legal requirements. By the way, many state agencies (including California’s Franchise Tax Board, Employment Development Department, and Board of Equalization) offer OICs as a tax resolution option if their applicable criteria are met.

Why did the IRS make this change toward being more understanding and offering additional opportunities to resolve controversies?

It is my opinion that the IRS recognized that many taxpayers were still struggling to pay their bills so they put in place common-sense changes to the OIC program that more closely reflected real-world situations. This expansion focuses on the financial analysis used to determine which taxpayers qualify for an OIC.

How did the program change the process?

In certain circumstances, the changes included:

• Revising the calculation for the taxpayer’s future income.

• Allowing taxpayers to repay their student loans.

• Allowing taxpayers to pay state and local delinquent taxes.

• Expanding the Allowable Living Expense allowance category and amount.

Other changes to the program include narrowed parameters and clarification of when a dissipated asset will be included in the calculation of reasonable collection potential. In addition, equity in income-producing assets generally will not be included in the calculation of reasonable collection potential for ongoing businesses.

How is the reasonable collection potential now calculated?

When the IRS calculates a taxpayer’s reasonable collection potential, it will now look at only one year of future income for offers paid in five or fewer months, down from four years; and two years of future income for offers paid in six to 24 months, down from five years. All offers must be paid in full within 24 months of the date the offer is accepted.

How do I apply or get more information?

Information about the OIC program, including applicant qualifications, how to apply, steps to complete the application process, Form 656-B, Offer in Compromise Booklet, and Form 656, Offer in Compromise, is available on IRS.gov.

NOTE: Even if you qualify for an OIC, it may NOT be the best solution! If you are close to the end of the 10-year statute expiration date, then other options may prove more advantageous – such as a status of currently not collectible (CNC), or a partial-pay installment agreement to wait out the expiration of the IRS collection statute of limitations.

If you do not feel comfortable pursuing this tax resolution yourself, contact me, and I will be pleased to discuss representing you or working with you as a consultant to guide you through it.

IMPORTANT NOTE ABOUT TAX RETURN PREPARERS

The IRS does NOT endorse any particular individual tax return preparer. For more information on tax preparers, visit the IRS website at http://www.irs.gov.

Do you use Turbo Tax or Tax Cut for your tax return preparation? If so, do you want a professional to look over what you have done to minimize the chance of error that could lead to an audit?

I have used Turbo Tax for helping family members for years (I use LaCerte for my return preparation clients due to licensing restrictions of Turbo Tax – and, of course, because LaCerte is a powerful professional product (very expensive, by the way….) with great diagnostics).

However, for basic returns, including some SMALL service-type businesses, Turbo Tax (and Tax Cut – the H&R Block product) can do a decent job. Having said that, it is very easy to answer a question wrong in the interview-format used by these products – and end up messing up a return fairly easily. I have had clients whose Turbo Tax (and Tax Cut) returns were audited, and the IRS proposed significant adjustments – including penalties and interest – because of errors attributable to the taxpayer’s lack of understanding of basic tax law. So, care must be exercised if you are going to file your own returns. For example, in the topic of RENTAL INCOME, Turbo Tax asks if the taxpayer qualifies as a real estate professional. Answering YES eliminates the test for the adjusted gross income (AGI) limitation. A client of mine erroneously answered that question “yes” and ended up owing a lot of tax, penalties and interest when the IRS challenged and disallowed (appropriately so ) his claimed status of being a real estate professional.

I offer a review service for those folks who want to try and save some money by using a self-help product like Turbo Tax – but want more peace of mind by having a professional – in particular, someone with extensive inside-the-IRS experience – look over the returns for any potential issues. For most individual returns, the review fee is $75. After making your payment, you save your returns as a PDF file and e-mail them to me. I will look through the returns (federal and state) and provide an e-mail analysis of the returns from an IRS perspective, together with suggestions as appropriate. If you agree that you need to make the changes I recommend, I will review your revised returns one more time at no additional charge. If you get in over your head, of course I can step in and prepare the returns for you, assuming there is adequate time remaining before the due date (for current year returns).

With over 30 years of IRS employment experience, I have extensive knowledge and understanding of IRS processes and procedures. This background will help me negotiate a resolution to your IRS or State tax controversy or get you through an IRS tax audit in the shortest time with the least financial impact. Effectively resolving a tax controversy, including the filing of and negotiating an IRS tax audit or IRS collection appeal on secured tax liabilities, can be – and often is – a very complex process where specialized knowledge and experience are critical to success.

Do your homework before selecting a firm to represent you!

I strongly recommend that you check out any individual or firm BEFORE you commit to having them represent you. Remember that it is YOUR LIFE – YOUR LIABILITY! You can delegate the AUTHORITY to have someone represent you. But, all tax agencies will deem YOU as solely responsible for your tax liability. Accordingly, you owe it to yourself to do some checking before retaining the services of a tax resolution specialist.

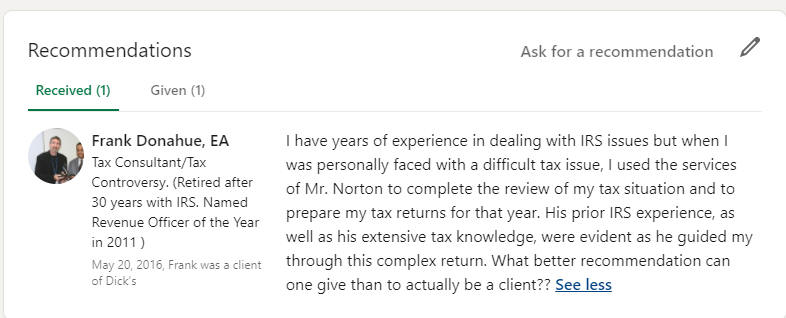

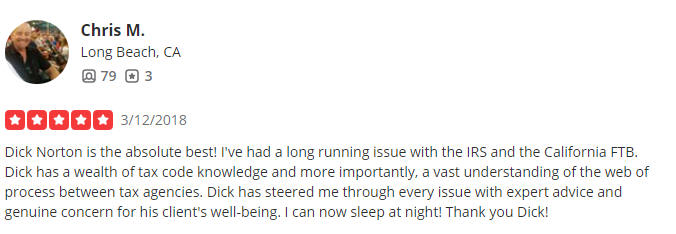

I have put some testimonials from my former clients on the website for your review.

Selecting the Right Person for your Situation

I STRONGLY suggest you be leery of any firm that advertises or claims to be #1 in the industry or to have the greatest level of success. The IRS frowns on companies or individuals making such wild claims, and has taken action in the past where firms have made such statements – even to the point of obtaining injunctions against their practice before the IRS.

Unfortunately, many firms make such unfounded claims as part of a scheme to attract and sign up clients. They often retain far more clients than they can effectively handle. These mass-market firms also tend to have a high turnover of employees, resulting in your case being shuffled from one employee to another – perhaps multiple times. Many clients of these firms end up forfeiting their retainers after they have become fed up with a lack of an effective tax controversy resolution service or audit representation, and just leave the firm to seek help elsewhere. Further, the lack of effective and timely responsiveness by these large firms creates frustration with the IRS Revenue Agent, Revenue Officer, Tax Compliance Officer, Appeals Officer, or Settlement Officer, or a State tax agent or officer, and that most often leads to further complications in the case.

I have personally taken over representation of a number of clients of these large representation firms who became very frustrated with the total lack of or poor quality of service from their representative or tax resolution specialist. In these cases, a significant part of my focus is doing damage control. That typically involves convincing the IRS employee that my focus is to facilitate the resolution of the tax controversy by providing timely and effective representation.

Many IRS employees have told me they prefer working with former IRS technical employees, as these representatives fully understand the administrative process and what is required to obtain an approved resolution of a tax audit or collection matter. When I was a Revenue Agent (early in my IRS career), I know that I appreciated working with former or retired IRS agents (at least most of the time – there were a few individuals I worked with who really should have pursued a different line of work after leaving the IRS…..)

One reference source for checking out a representative is www.ripoffreport.com. It is a website where former clients of tax resolution firms have taken their time to share their experiences with the firms they selected to represent them in their tax controversy. Once you have identified a firm for potential representation, do a Google search for the company with the term “review” – it may bring up additional information that you need to consider. You can also check the Better Business Bureau for ratings. One of the former large firms near me (for whom I took over some of their clients over the years) has a “D-” rating. You really need to ask yourself whether you would want a company with such a dismal rating handling a matter that could seriously and adversely affect your financial life!

I strongly suggest you carefully research each company you are considering retaining BEFORE you make your final decision. Making a bad choice could not only cost you money, but could lead to more serious issues with the tax agencies – especially when the company fails to be diligent and timely in their communications with those agencies.

Once again, it is my firm opinion that a taxpayer should be skeptical of any firm’s or individual’s unsupported claim that they are a “leader” in the industry, or makes promises that sound too good to be true (such as, “We get our clients settlements that are pennies on the dollar”). That often repeated scenario generally refers to an “offer-in-compromise” – or “OIC” for short. It is a program wherein the IRS (and many states as well) will accept an amount less than what is legally owed to settle an account. I still hear and read about such wild claims in the media far too often! When I was still working for the IRS, our staff would encounter cases prepared by some of these firms that were – well, no other way to say this – garbage! It was a royal waste of our time and the taxpayer’s money for the taxpayer to even pursue an OIC resolution that had no hope of success.

What About an Offer In Compromise (Settling your debt for less than the face amount)?

Since I mentioned OICs, there are strict guidelines that must be met to even qualify for an offer in compromise (OIC). In my experience as an Associate Chief in Appeals (accepting or rejecting these OICs on behalf of the Commissioner) and in client representation post-retirement, a very small percentage of the accepted offers are resolved for a “few pennies on the dollar”; however, all accepted offers do result in some relief of the amount owed.

Statistically, in 2017, I read that the IRS accepted just 40% of the OICs submitted. A significant number of these were modified; however, the IRS counter-offered the taxpayer a typically higher offer amount before approving the OIC, and the taxpayer accepted the revised amount. Even after the offer was revised, the taxpayers ended up settling their debt for less than its face value.

Substantial concessions of tax, penalties, and interest by the IRS and state agencies generally require extenuating circumstances – such as serious medical issues, advanced age, or actual or projected long-term unemployment by unskilled individuals. I was the approving official at the IRS for offer in compromise (OIC) cases in my jurisdiction for almost two decades, so I have a solid understanding of what is required to potentially get an offer accepted.

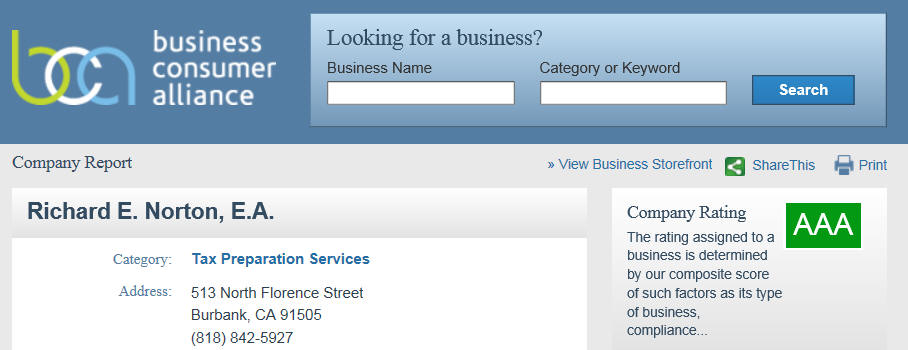

As I mentioned before, I recommend that you check the Better Business Bureau before making a final decision about retaining a tax resolution specialist. Here is the link to my accredited BBB A+ report:(our former address is displayed on their website):

Another company rating service is provided by Business Consumer Alliance. Here is their assessment of my firm:

I recommend checking out any company you are considering through these two consumer services.

Important! If you have just received a Notice from the IRS, FTB, or any other State tax agency, please – do NOT ignore it! Some of these notices have very specific time frames within which you can appeal a proposed action. For instance, Letter 1058 issued by the IRS warns a taxpayer that if they do not pay the amount due, or file an appeal, within thirty (30) days of the notice date, the IRS WILL enforce collection (that means levying (seizing) bank accounts, wages, etc.). Unfortunately, a number of my clients waited to contact me AFTER the 30-day period had expired and the IRS had levied their bank account or taken their paycheck! By waiting too long, these clients lost a very valuable appeal opportunity! Usually, I can get the levy released, but the levy could have been avoided in the first place! Please – don’t procrastinate and forfeit your right to appeal a proposed IRS enforcement! Allow me to negotiate an acceptable repayment plan or offer in compromise on your behalf. Help is just a phone call or email away! Expecting a tax refund on your current year Federal return? Have you NOT filed a past return? The IRS has begun HOLDING REFUNDS for taxpayers with unfiled returns! The IRS Notice you may receive requires you to file the delinquent returns BEFORE the refund check is released (assuming you have no liability on these delinquent returns). If you do NOT file the delinquent returns, the IRS will prepare returns for you (called a Substitute for Return, or SFR for short). There are NO deductions (other than the standard deduction) computed by the IRS in an SFR return – meaning, you likely will be paying MORE tax than you really owe! It is important to realize that you WILL lose your right to a tax refund if you file a delinquent return more than 3 years after its original due date. Have you recently changed your legal name (typically as a result of a marriage or divorce)? Remember to contact the Social Security Administration BEFORE you file your next tax return to have your name corrected. The IRS matches the Social Security Number and Name (first and last) as reflected on your tax return against the Social Security database. If there is no match, the processing of the tax return may be delayed. To make the change, complete and file Form SS-5 that is available on the Social Security website (www.ssa.gov).

Some Useful Information

![]()

|

STANDARD MILEAGE ALLOWANCE RATE UPDATE |

2024 standard mileage rates

| Beginning on Jan. 1, 2026, the standard mileage rates for the use of a car (also vans, pickups or panel trucks) will be:

· 72.5 cents per mile for business miles driven, up from 70 cents (an increase of 125 cents per mile from the 2023 increase) · 20/5 cents per mile driven for medical or moving purposes · 14 cents per mile driven in service of charitable organizations (no change to this rate) |

2023 standard mileage rates

Background Information

When you first buy a car and use it for your business, you have the option to use the standard mileage allowance or actual expenses. To use the standard allowance, you MUST use it in the first year you began using the car for business. You can switch to ACTUAL later. However, with fluctuating fuel prices, the ACTUAL method may yield greater tax savings. The standard mileage rate may not be used for a purchased auto if:

- it was previously depreciated using a method other than straight-line for its estimated useful life;

- a Code Sec. 179 expensing deduction was claimed for the auto;

- the taxpayer depreciated it using MACRS under Code Sec. 168; or

- the vehicle is used for hire, such as a taxicab. (Rev Proc 2006-49, Sec. 5.06)

Also, the standard mileage rate can’t be used to compute the deductible expenses of five or more autos owned or leased by a taxpayer and used simultaneously (such as in fleet operations). (Rev Proc 2006-49, Sec. 5.06(1)(b)).

A taxpayer who uses the mileage allowance method for an auto he owns may switch in a later year to deducting the business connected portion of actual expenses, so long as he depreciates it from that point on using straight-line depreciation over the auto’s remaining life. The depreciation deductions would still be subject to the Code Sec. 280F dollar caps. (Rev Proc 2006-49, Sec. 5.06(3))

A taxpayer may use the mileage allowance method for a leased auto only if he uses that method (or a FAVR allowance method) for the entire lease period (including renewals). If the lease period began before ’98, this rule applies only for the post-’97 portion of the lease period (including renewals). (Rev Proc 2006-49, Sec. 5.06(2))

Both methods require that you maintain good records (e.g., a log) that support your claimed annual TOTAL, BUSINESS, COMMUTING, and other PERSONAL miles. The sum of your business, commuting and personal miles must equal your TOTAL miles. Keep all repair, tire replacement and maintenance receipts to prove your expenses. Those documents also establish your odometer reading at the time of each service.

BE AWARE OF IRS RELATED SCAMS!!!!!

There are many emails circulating that appear to be from the IRS. I have personally received a number of these scam emails. They tell you about alleged unclaimed refunds, stimulus payments, or other items that require you to submit your personal information – such as Social Security Number, credit card information, etc. – to get the money or other benefit. According to the IRS, the origin of these emails is usually a foreign country.

The IRS NEVER sends out unsolicited E-mails to taxpayers. Period. All IRS communications are by mail, or by FAX (and – fax communication will occur after you have established contact with the IRS and provided them with your fax number and authorization to use it).

Please be very cautious when you receive any unsolicited E-mail asking for your personal or financial information from the IRS – or for that matter, from any source! Most of these fraudulent E-mails “steal” the logos and website designs of legitimate companies – such as PayPal, banks, savings and loans, and other institutions – including the IRS! They appear legitimate, but they are NOT!

TELEPHONE CALL SCAMS!!!! Wow – this has become a MAJOR issue. Personally. I have received many calls from crooks who represent themselves as officers of the IRS or the Treasury Department and threaten arrest or other enforcement actions unless immediate payment is made. Of course, I can quickly identify these people – and actually have some fun scaring the daylights out of them! But far too often, they get a senior citizen on the phone who lacks awareness that these scammers are impersonating an IRS employee. I read far too often of our seniors losing thousands of dollars! So please – spread the word among your family and friends! The IRS NEVER – repeat – NEVER calls and threatens over the phone that they are going to arrest someone. If you get such a call and are concerned about whether it is legitimate, get their name, position, office location, and contact number, and feel free to contact me. I can very quickly determine if it is a scam. You can also put the call-back number into GOOGLE – often, others have received calls from that number and will share their experience. Most of these callers (from my experience) are using a product like Magic Jack. It allows them to pre-program the CALLER ID to display a 202 area code (Washington, DC), as well as a name similar to US GOVT. In recent times, they have become more clever and are using area codes in the vicinity of their intended victim.

Be careful, folks. I do not want any of you falling victim to a scammer!!! One of my clients told me of their younger sister getting caught up in one of these scams. She ended up giving the crook just over $10,000 – the amount she had saved for her college tuition! It was a heartbreaking story!

What Can I Do For You?

With today’s technology, I can assist clients with professional tax audit representation, tax collection representation, consultation, and return preparation services throughout the United States and abroad! As an Enrolled Agent licensed by the United States Treasury Department, I am authorized to practice in all 50 states, and to represent taxpayers worldwide regardless of where they live. I have represented and assisted clients living in other parts of the world (either U.S. citizens living abroad or foreign nationals with U.S. property interests or income) such as Saudi Arabia, Australia, India, Belgium, and Great Britain.

Remember that the help you need from a Tax Resolution Specialist offering tax services for the resolution of your IRS or State tax controversy or tax audit, any form of IRS appeal, or preparation of your current or delinquent income tax returns, is just an email or phone call away! If you need help with:

- tax return preparation

- tax consultation

- tax resolution services – providing tax controversy resolution (IRS tax audit help or tax problem help and representation, including an administrative appeal, IRS tax collection representation, or Franchise Tax Board (FTB) or Employment Development Department (EDD) audit or collection problem resolution)

- IRS expert witness (for mitigation/arbitration/litigation)

Then I encourage you to read the extensive content on this website.

My Prior IRS Experience

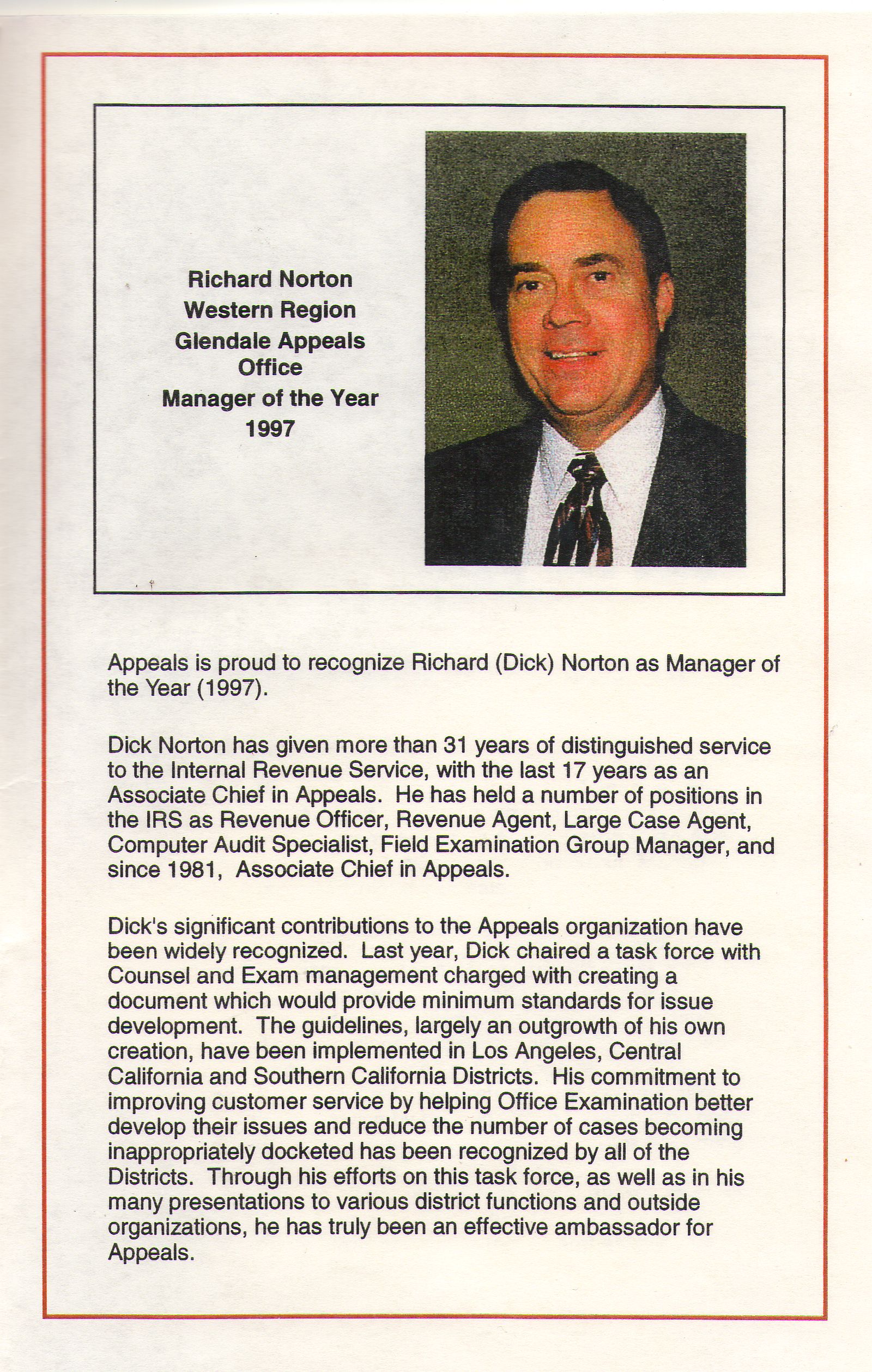

I retired in September 2000 as the Associate Chief of the Los Angeles, California, IRS Appeals Office, following many years in managerial and technical positions in the IRS Appeals, IRS Examination, and IRS Collection functions. I have extensive inside-the-IRS experience in three operations/divisions (Collection, Examination, and Appeals) that a limited number of other practitioners possess. As evidence of my success and recognition while working for the IRS, I was awarded the National Appeals Manager of the Year Award in 1997.

This extensive knowledge of IRS policies, procedures, and practices has proven invaluable in resolving my clients’ tax issues. I often provide guidance or services to other tax professionals who are facing challenging technical or procedural issues.

The primary focus of my practice is representing clients in IRS tax audits or IRS collection disputes, as well as in IRS administrative appeals of tax collection or audit controversies, and in other tax issues. While the IRS is my primary focus, I also represent clients in State income and employment tax controversies.

As mentioned before, I offer consultation services to guide clients who choose to represent themselves in resolving or settling their IRS, state income tax, or employment tax controversy. This service is primarily intended to help taxpayers who cannot afford full representation but need assistance with IRS tax audits, collections, or appeals, or other guidance in negotiating the resolution of their tax controversy. If my clients – while trying to represent themselves with my consultation assistance – suddenly find themselves in over their heads, I can quickly step in and represent them in resolving their tax controversy.

Need an expert witness?

If you are involved in litigation with your preparer/representative, the IRS, or litigation related to IRS practices and procedures, and you are in need of an expert witness intimately familiar with IRS collection, examination, and appeals functions and their procedures, then please contact me. With 34+ years of IRS service and experience in the IRS Collection, Examination, and Appeals Divisions, I am well qualified to testify concerning IRS procedures and practices, and possible malpractice by other professionals before the IRS. I have given testimony as an expert witness in the California Superior Court.

GENERAL DISCLAIMER

| Nothing on this website is intended to be specific tax advice for you, the reader, and cannot be relied upon for the purpose of avoiding any penalty that may be imposed by the IRS or any tax agency. The material on this and all other pages of this website is provided for informational and educational purposes only. I do not guarantee or warrant in any manner the suitability, usefulness, accuracy, timeliness, or results of any portions of this site, nor the links contained in this site which link to other areas. At times, information is taken from other sources and is believed to be accurate, but no verification or confirmation is performed. Tax law is a very complex subject. Any tax opinion upon which you may rely requires the careful and thorough analysis by a tax professional of the specific facts of your situation and the applicable legal statutes. If you need specific advice, then you should request formal tax consultation, as its purpose is to provide you with guidance for your specific tax issue or question upon which you can rely. |

Former IRS Collection, Audit and Appeals Positions

To give you a better understanding of my qualifications, I want to spend some time discussing my thirty-four plus years in technical and managerial positions with the Internal Revenue Service (IRS).

During my extensive and successful IRS career, I gained valuable experience in the following positions within the IRS Collection, Examination, and Appeals Divisions:

-

Revenue Officer (IRS Collection Division)

- Acting Collection Office Group and Field Manager positions

- Revenue Agent (IRS Audit Division)

- Classroom and on-the-job training Instructor for Revenue Agents

- Employment Tax Specialist

- Large Case Team Revenue Agent

- Computer Audit Specialist

- IRS District Conferee (in the former IRS District Conference Staff that merged with Appeals)

- Field Examination Group Manager (in the former West Los Angeles and Hollywood IRS Offices)

- Associate Chief of the Los Angeles and Glendale Appeals Offices (IRS Appeals)

- Acting Regional Director of Appeals for the Western Region

The many technical and managerial positions I held within the IRS provide me with in-depth knowledge of tax law, as well as the policies and practices of the IRS Audit, IRS Collection, and IRS Appeals Divisions. In representing you in the professional resolution of your tax controversy – whether an IRS, FTB or other State audit or collection matter, my experience of having been on the “other side of the table” enables me to guide you through the maze of the IRS and other agency collection, examination and appeals processes. My objective, as a Tax Resolution Professional and your representative, is to use my extensive tax law knowledge and decades of IRS experience to negotiate a favorable resolution of your IRS, California, or other State audit or tax collection controversy case.

To represent you before the IRS or the State of California taxing authorities (FTB and EDD, or an appeal of an income tax issue before the BOE), your tax resolution professional must be an Enrolled Agent (EA), Attorney, or CPA. CPAs and Attorneys are licensed by individual States (and while they usually practice within those states, they are authorized to represent taxpayers in any state). Enrolled Agents are licensed by the United States Government (United States Treasury) and represent taxpayers in any of the 50 states as well as internationally. Further, Enrolled Agents are tax law specialists. Only a percentage of attorneys and CPAs specialize in assisting clients with resolution of a tax controversy in an IRS, FTB, or other state income tax, employment tax, or other type of tax audit or tax collection situation.

Why select me for the resolution of your tax controversy?

You may already have visited numerous websites in search of the right person to represent you or prepare your returns. There are literally thousands of practitioners offering tax resolution services, tax settlement, and tax return preparation services. Many of these practitioners are very competent and worthy of your trust and business. Others have no business taking your money when they lack the skills, knowledge, ethics, and/or commitment to do the absolute best job in representing or advising you. In fact, if you used one of these individuals, your situation could become much worse!

In fact, one national firm had been the subject of a major investigation. You can watch the ABC special video report here: http://abcnews.go.com/Blotter/video/taxmasters-investigation-13383312. One former employee of this firm alleged that the company had hired numerous salespeople to “sell” its services, yet failed to hire sufficient technical staff to handle its existing client base.

This type of situation WILL make matters worse for their clients as the tax agencies expect and demand timely responses. I have taken over clients from several large firms in our area, who told me they were “ignored” by the firms’ employees. As a direct result, the IRS and other tax agencies became frustrated and more aggressive – stepping up their enforcement efforts.

Take your time and exercise care in selecting the right representative. There are many good, competent, and ethical individuals and firms. Unfortunately, many others will simply take your money and fail to deliver. Do your homework on the Internet by researching sites like Ripoff Report, the Better Business Bureau, and others using search terms such as “tax resolution.” If you have a particular firm in mind, type in the name of the firm and the state. Be leery of companies with a lot of complaints – even if those complaints appear to have been adequately addressed (responded to) by the company. Folks generally will not take the time to write an adverse rating unless they are really upset.

While I was still working at the IRS, my staff and I encountered all types of representatives. If a practitioner was really incompetent, we would contact our Washington, D.C. Office of Professional Responsibility (formerly called the Director of Practice) to recommend disciplinary action – including, where warranted, that the individual be barred from representing clients before the IRS. An incompetent representative not only fails to assist their client in resolving a tax controversy but often makes matters worse for the taxpayer.

Determining who you should trust with your financial affairs is a major decision that you should not take lightly. I can suggest five reasons why I believe I merit your trust and confidence to help you with your IRS, FTB, EDD, or other tax agency audit, appeal, tax controversy, or return preparation needs.

|

1. EXPERIENCE AND KNOWLEDGE |

First, I have in-depth tax law and procedural knowledge and inside-the-IRS experience to effectively represent you. I understand how the Internal Revenue Service works internally, and that allows me to predict how they most likely will approach your particular tax controversy, and even more importantly – how best to get you the least costly resolution or settlement of your tax controversy problem case. I know the responsibilities and settlement authority of all categories of IRS employees. I do not waste my time (or my client’s money) discussing matters with employees who lack the authority to resolve a particular controversy. State tax agencies operate similarly to the IRS, so my extensive IRS background assists me in working with employees from those other agencies such as the California Franchise Tax Board (FTB).

|

2. PERSONALIZED SERVICE DUE TO LIMITED CLIENT BASE |

Second, I limit the number of clients that I represent. This ensures that you will always have quick access to me. Think of this scenario. You open your Saturday mail and find a threatening notice from the IRS. Understandably, you are very concerned and want to talk now – not later – with your representative about this notice. With most representation firms, you will likely be unable to talk to anyone until the following Monday (and that assumes the individual will return your call at that time…).

As my client, you will have my home and cell numbers so you can call me anytime you need to discuss an urgent matter regarding your case. I access my e-mails almost hourly, both during the day and in the evening – seven days a week. For example, if you receive an unexpected threatening IRS Notice in Saturday’s mail, we really should discuss it that Saturday – not the following week. Scan and email (or fax it) to me. I will then explain what it means and how I plan to deal with it, so you do not spend the weekend stressed out and unable to sleep or concentrate at work.

As my existing and former clients will confirm, I am almost always available 7 days a week – from early morning until late at night. I tell my clients that I do not want them stressed out over a weekend or holiday because of concern about something like an IRS tax notice they need to discuss with me. I ask them to email or call me so I can explain the Notice to them and assure them that I will take whatever action is required on Monday morning.

Comments I have heard from former and current clients (who left other representatives to have me represent them) convince me that immediate availability and responsiveness are seldom attributes associated with large production-mill firms. Almost all of these firms advertise extensively on the Internet and occasionally on television or in other media such as radio. They are lightning-quick to take your hefty retainer, but then – good luck on getting them to actually help you with your tax controversy.

Here is something for you to consider. If a tax resolution company requests a very large payment up front (many thousands of dollars, for example), that may be a big warning sign to you – particularly if they offer to represent you for a flat fee. Consider this. Once they have all your money, there is NO financial incentive to provide services to you (does this sound like some HMOs?). Most reputable firms I know in our line of business will ask for a reasonable retainer up front and then bill you for the services provided in the tax resolution of your case.

If you are paying for representation, you, the client, have every right to expect timely response to your inquiries and actions on your case. That often does not happen in large regional or national firms where each employee is burdened with an unreasonable number of client cases. Former clients of those firms who left (often forfeiting large retainers) and then retained me have shared their frustration at being unable to reach their appointed representative after leaving numerous voice messages or emails. As a last resort, they go up the chain of command to their representative’s superior, hoping for (but seldom receiving…) a resolution of their problem.

If you have been calling one of these firms to discuss representation and not receiving a timely call-back, that should be an immediate and serious warning to you. Once they have your retainer, their practice may be to ignore you and focus their efforts in finding and signing up even more clients – in spite of the fact they have a fraction of the resources required to timely service all the clients who have retained them!

If you are currently involved with one of these large firms, have paid a large non-refundable retainer, and are receiving inadequate service, you may wish to retain me as a consultant to assist you in getting your firm to do the right thing on your IRS tax audit, appeal, or other IRS, FTB, or other state controversy or problem. You do need to exercise caution when deciding to simply walk away from an existing representation engagement. Many professionals have early termination clauses or forfeiture-of-retainer provisions in their Engagement Letters. Rather than lose your retainer, use my knowledge and experience to make them do the right thing!!!

In my opinion, I pose a serious threat to any firm that is negligent in its fiduciary responsibilities to its client. I have given defense testimony in the California Superior Court as an expert witness in a multi-million-dollar lawsuit alleging civil malpractice by a CPA. Use my experience and knowledge to your advantage if you have already paid a significant sum to a representative and you feel that they are not meeting their fiduciary responsibilities to you!

Whether you retain me or some other professional, my recommendation is to stay clear of the large production-mill firms. Many have testimonials on their websites quoting a few clients for whom things went right. Do not stop there! I recommend you do some Google research on the firm. You will likely find extensive negative feedback from their other clients. The Better Business Bureau is also a good source of information on these firms. For instance, here is a link to one of their reports on a large firm that does extensive advertising but (per the BBB) allegedly fails to deliver on its promise. I do not know if the firm has “cleaned up their act” or not.

One other point – if you retain my services, you and the tax agency will be working solely and directly with me – not an associate, paralegal, or clerical type. In the large firms, you most likely will be working with an employee who may or may not possess the qualifications and experience to effectively represent you. Furthermore, as I have heard, one of the large firms in my geographical area can experience extensive staff turnover.

There are a number of membership organizations that tax resolution specialists (EA’s, CPA’s, and Attorneys) can join. For example, in addition to the basic United States Treasury licensing requirements, membership in the California Society of Enrolled Agents (CSEA) (or similar organizations of other States), and the National Association of Enrolled Agents (NAEA) means that the EA has met continuing educational requirements beyond what the US Treasury requires.

Any taxpayer seeking help should value a professional who continually strives to keep their skills sharp and current to provide the best possible representation. In keeping with this objective, I am a long-standing member of NAEA (National Association of Enrolled Agents) and CSEA (California Society of Enrolled Agents), and a former member of NATP (National Association of Tax Professionals).

What I believe is important for your consideration is:

(1) that your representative is properly licensed,

(2) is an active member of recognized professional societies,

(3) has the technical skills and experience to maximize the probability of a cost-effective tax controversy resolution, and

(4) has no or very few complaints made to the Better Business Bureau or other rating sites.

Everything else being equal, I suggest that a representative who has had extensive and successful experience within the Internal Revenue Service should have a better understanding of the inner workings of that agency, including its directives, policies, and procedures, and thereby would have a higher probability of negotiating a more expeditious and favorable resolution of a tax controversy. Again, this is strictly my opinion – and a factor you need to weigh in making a decision for representation.

I do need to state for the record that past employment with the IRS (or a State tax agency) is NOT a guarantee that the individual is best suited for your particular tax dispute. In fact, I have encountered a few former IRS employees – both while I was still working for the IRS and post-retirement – who I believe have no business representing taxpayers. By the same token, I have experience in meeting and working with some representatives who are very skilled and competent in IRS and State collection and audit representation who have had minimal or no inside experience as an IRS, FTB, or other state tax agency employee.

Finally, my clients appreciate that I am available most nights and on weekends for priority matters. As stated previously, my clients have my personal cell and home phone numbers so they can always reach me to assist them with any emergency (such as a Notice of Levy or Federal Tax Lien that arrives on a Saturday). This level of access gives my clients peace of mind knowing that I am just a quick phone call or email away. You will have to decide just how important it is to have immediate access to your professional representative in pursuing the prompt and effective resolution of your IRS or other agency tax controversy! Most practitioner offices are closed after hours and on weekends, with limited or no means to contact your representative.

|

3. COMPETITIVE FEES |

Third, my service fees are among the lowest in the industry. Why? Here are some reasons:

I keep my costs down by minimizing advertising costs and expensive office space. My clients come through this website (which ranks highly on Google and other search engines) and by referrals (often from other practitioners who have a client who needs my level of experience).

I utilize very high-speed computers, super-fast Internet access, LaCerte tax software, and a comprehensive online tax research service that reduce my time in providing tax services for tax resolution (representation), return preparation, and tax research. I also subscribe to Core Logic Research (formerly Data Quick) – a research service IRS and often State employees use to review a taxpayer’s public records. I am authorized to access the IRS database (through eServices) and the FTB online database directly. Quick access to IRS and State tax information about your account is important. On this last point, wouldn’t you agree that it is critical that your representative know what the IRS knows about you when negotiating the resolution of your tax case?

I recommend that you ask other representatives you are considering for retention – “What research services do you subscribe to in your practice?” If they do not subscribe to a high-end service, then I would recommend you continue looking. While purchasing this level of sophisticated research access is expensive, the bottom line is that these great products enable me to resolve cases more quickly (saving me time – and you fees). This reduces my overall costs to provide representation. I have selected Parker Tax Library for my practice because of its extensive, up-to-date content, high level of support, and competitive pricing.

Lastly, I have a comfortable retirement pension from the IRS, so I can afford to keep my fees down, since representing clients is not my sole source of livelihood.

|

4. Client Participation Encouraged in the Process to Reduce Representation Costs |

Fourth, I encourage my clients to do as much of the preparatory work for their case as possible (following my guidance). Why pay me (or any other professional) to create adding-machine tapes of receipts or to fill in basic information on forms? You should NOT have to pay a professional to do these simple tasks! What you need tax resolution assistance for are the following:

- in an IRS or State collection tax controversy resolution,

- for ensuring (by a thorough review) that documents are properly completed, consistent in their content, and present your financial situation in the best possible light for your benefit, and/or

- in negotiating a tax controversy resolution of your collection deficiency for the lowest required amount for an offer in compromise or installment agreement;

- in an IRS or State audit tax controversy resolution,

- that your evidence sufficiently supports the deductibility of an expense or the allowance of a tax credit, or

- that your reported income is accurately calculated, or

- that the non-taxability of a deposit or transaction is accepted.

Many of my clients have significant liabilities with the IRS or other tax agencies – and often hefty debts with other creditors. The absolute last thing they need are expensive representation fees to add to their financial burden. Therefore, I strive to find ways to help clients conserve their precious resources by encouraging them to do as much “leg-work” on their own case as possible. That minimizes the fees they have to pay for my professional services in tax representation/tax controversy resolution.

One way I accomplish this for my tax controversy clients is by providing them with both the required and current PDF fill-in forms, along with guidance on their completion. Once my client completes and emails me the forms, I carefully review them for errors and inconsistent or unclear entries, and then work with my client to make any necessary changes or provide additional attachments I deem necessary to ensure favorable acceptance by the tax agency.

I want to stress that all of my clients work EXCLUSIVELY WITH ME – not with an assistant or clerk. That is not a standard practice in the industry with large firms. The CEO, CFO, or other head person for a firm may be well qualified; however, it is unlikely (in my experience) that they ever will be personally involved in your case – unless something goes terribly wrong and you end up complaining. So, I suggest that is a factor that you need to carefully consider.

My clients appreciate the opportunity to minimize their total cost for my services to just those specific areas (such as face-to-face or over-the-phone negotiation with the IRS or a State agency) where they really need my skills to resolve their tax controversy.

|

5. Focused on Continuing Education with Powerful Research Resources |

Finally, it is important that your representative keep current on new tax developments – legislation, litigation, and tax agency procedural changes. I receive periodic updates (tax law changes, court decisions, tax agency procedural changes, etc) in the areas of my practice so that I can continue to provide the best possible service to my clients. I also subscribe to Data Quick, an online service that provides invaluable information to help resolve tax disputes. Without these tools, no representative (in my opinion) can effectively represent you before the IRS – or any other tax agency.

In addition to this research service, I have often attended the annual CSEA Super Seminars. This is an outstanding opportunity for me and many other EA’s, CPA’s, and attorneys to keep abreast of the latest trends, laws, and procedural updates through presentations from highly respected tax attorneys and other professionals from around the U. S. I also am an active member of the National Association of Enrolled Agents and the California Society of Enrolled Agents. These organizations provide valuable materials, updates, and resources that help their members deliver effective representation and guidance to their clients.

I hope these five reasons merit your confidence in my ability to effectively represent you in your IRS or State tax controversy, or to provide you with tax preparation or consultation services. I take my representation responsibilities to my clients very seriously. Much of my practice is based upon referrals. Working closely and effectively with clients to achieve the best possible resolution or settlement of their tax controversy is the most effective means of growing a business based on client recommendations.

Tax Practice Areas

The four broad categories of services that I offer are:

- Tax Return Preparation

- Tax Controversy Resolution (providing irs tax audit help or resolution of an IRS tax audit or collection matter)

- Consultation

- Expert Witness

Tax Return Preparation

There are many self-help income tax return preparation products on the market today for preparing your 1040, 540, and other tax returns. Some of these products are actually quite good – particularly if you have some basic understanding of income tax law. Two of the better-known products use the interview technique to guide users through preparing their own income tax returns for the IRS and their State.

While the interview concept is generally effective, errors remain due to the technical complexity of some interview questions. An incorrect response could result in the erroneous reporting of one or more transactions, which could lead to an audit that, in turn, will likely result in additional tax, penalties, and interest, as well as representation fees for the resolution of the income tax controversy.

To illustrate a complexity of the law, here is a simple – but not uncommon – situation. If you receive a piece of property from a relative – by gift or bequest – do you know what your basis (cost value) will be when you sell it? Your cost basis will differ depending on whether you received it as a GIFT or by INHERITANCE. If by mistake you use the wrong basis, you will either pay too much income tax (which the IRS or FTB likely will keep unless you find out about the error and file an amended return within the statute of limitations period), or pay too little tax and end up owing the IRS/FTB a bundle (including interest and penalties) when they catch up with you for an audit.

The tax resolution specialist fees associated with defending you in the resolution of a tax controversy before the IRS or FTB because of errors in your income tax return most likely will end up costing you many times the savings you believe you will achieve by preparing your own tax return.

You also need to be aware that selecting a low-cost service that cranks out income tax returns like a puppy mill may result in adverse financial consequences for you if your tax return is inaccurate. Some of these firms get targeted by the IRS (if the firm makes an unacceptably high number of errors on clients’ returns that are discovered during return processing or audits), and then ALL of their clients get audited! My advice to you is to stay clear of firms owned or managed by an individual who is NOT an E. A., CPA, or Tax Attorney.